Price Suppression

What Is Driving This Bear Market?

Dear Bitcoiners,

In last week’s newsletter we discussed institutional adoption based on the latest 13F filings, including the top 25 institutional ETF holders. This week, discussions circulated on social media about alleged price suppression by Jane Street, #1 on that list and currently the largest ETF holder.

These claims gained traction after a lawsuit involving Jane Street became public, alongside renewed attention on the firm’s past industry links, including connections to figures and firms associated with both FTX and Terra. Both collapsed during the 2022 bear market and caused significant damage across the industry. In this newsletter, we’ll look at the mechanics of the Authorized Participants (APs), such as Jane Street, and how they actually interact with the Bitcoin ETF system.

Price Suppression

APs are the firms responsible for creating and redeeming ETF shares, helping keep ETF prices aligned with their underlying assets. The rumors suggest that Jane Street, as an AP for Bitcoin ETFs, may have used a systematic trading strategy, the so-called “10AM algo”, when ETFs open, allegedly adding sell pressure.

Under normal market mechanics, if an ETF trades below its net asset value (NAV), arbitrage should close that gap by pushing prices back toward equilibrium. In practice, however, APs can hedge exposure using futures or other derivatives rather than immediately trading spot Bitcoin. This means spot demand can sometimes be delayed, netted internally, or sourced off-exchange. The arbitrage mechanism still functions, but it does not always translate into immediate spot buying pressure. That can affect timing, though it is not the same as permanent price suppression.

Additionally, in-kind creation and redemption adds flexibility. Instead of delivering cash that must then be used to purchase Bitcoin, APs can deliver Bitcoin directly, sourced from counterparties of their choosing. This removes the need for immediate on-exchange buying and allows exposure to be managed with less visible market impact. The ETF still ultimately holds real BTC, but the process can reduce short-term buying pressure in public markets.

Many institutional purchases also occur through OTC desks, which existed long before ETFs. OTC trades usually have less immediate impact on exchange prices, although dealers may hedge positions on public markets. Without OTC markets, more of that flow would likely hit exchanges directly, potentially increasing volatility.

Unlock full access to the Bitcoin Strategy Platform, including all top-tier indicators and full newsletter content. Sign up today and claim a 25% LIFETIME discount!

The rise of ETFs, trusts, and custodial lending platforms does increase synthetic or “paper Bitcoin” exposure in the system. While ETFs themselves hold real BTC in custody, APs can hedge using derivatives. Lending markets may also rehypothecate BTC held in custody, increasing synthetic exposure overall.

👉 Key Insight: When derivatives are used instead of spot, the risk does not disappear, it simply moves elsewhere in the system. These effects tend to influence timing rather than long-term price direction.

It’s important to remember that synthetic BTC is not real BTC, it represents leveraged or offsetting positions somewhere in the system. Someone ultimately carries the risk. We saw that in 2022 with Terra and FTX. In the short term, derivatives and synthetic exposure can influence price and sentiment. But over the long term, excessive leverage tends to unwind. While short-term damage can occur, these periods have historically created some of the best long-term entry points for those focused on holding real BTC.

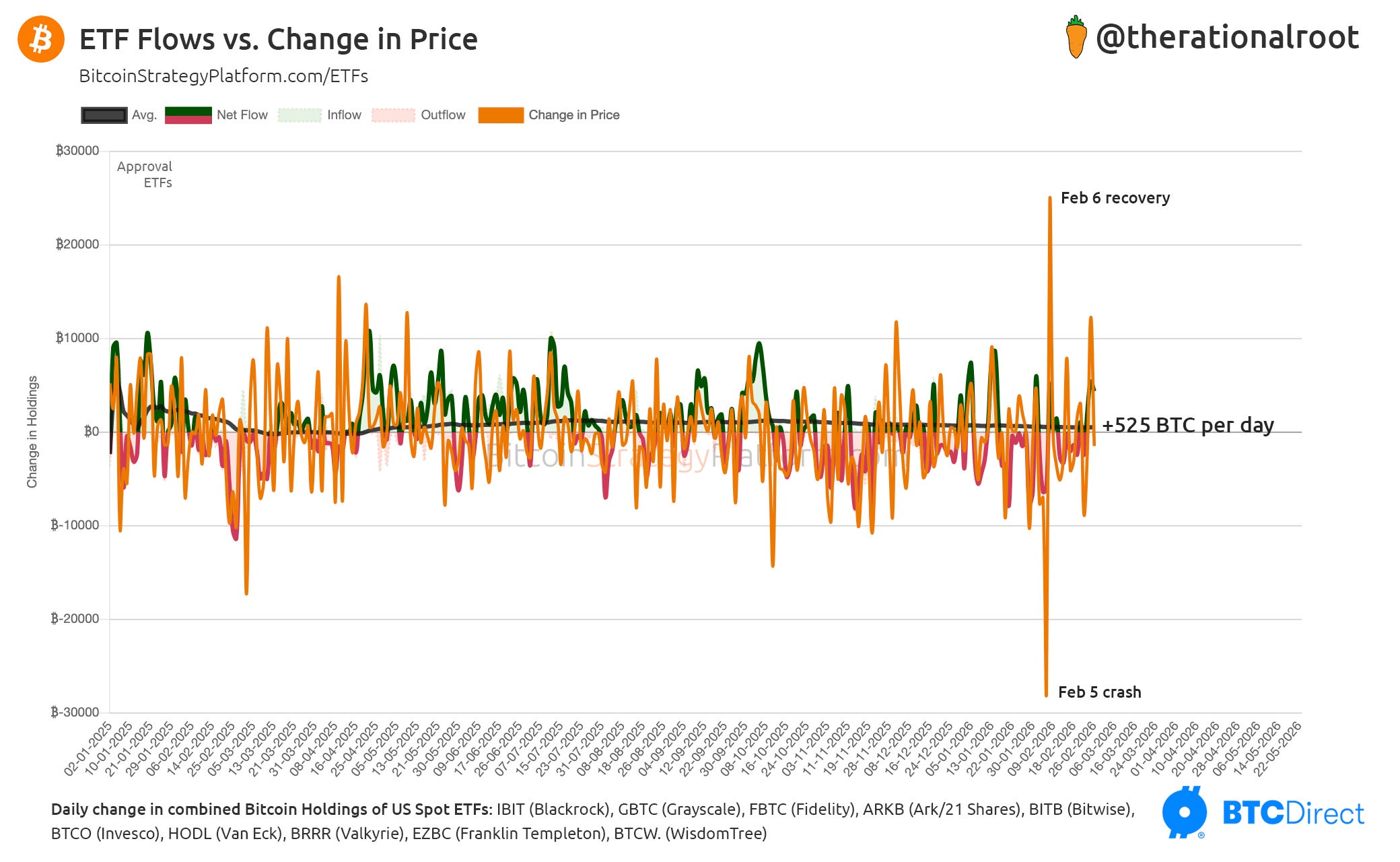

In the chart below we compare ETF flows with Bitcoin’s price change.

👉 Key Insight: There is a strong correlation between ETF flows and price change, suggesting ETF demand does translate into real market impact, challenging the idea of sustained structural suppression.

To conclude, market makers can influence short-term price action, potentially dampening moves in both directions. But when Bitcoin underperforms, “manipulation” is frequently used as a convenient explanation. These mechanics are unlikely to be the primary driver of the broader bear market.

So what is driving this bear market? Let’s look at the real forces behind it.